Stop throwing money away on a vehicle that’s already gone. If your car is at the scrap yard, every day you wait to cancel your policy is cash down the drain. You need to know how to cancel car insurance after junking a car correctly to avoid an insurance lapse that spikes your future rates. In Michigan, where the average annual cost for full coverage is $3,200 in 2026, making a mistake during this transition is expensive.

We know the Michigan SOS paperwork is confusing and the fear of a coverage gap is real. This guide explains the exact steps to stop automatic payments immediately and secure your prorated refund without facing state fines. You’ll learn how to handle your license plate and title transfer so you can walk away with cash in your pocket and a clean driving record today. We’ll cover the 50/100/10 minimum requirements and the specific sequence you must follow to stay protected and get your money back fast.

Key Takeaways

- Learn why you must wait until the tow truck leaves before calling your agent to avoid liability issues.

- Discover exactly how to cancel car insurance after junking a car using your mobile app or agent without triggering a coverage lapse.

- Understand the Michigan SOS requirements for removing license plates and notifying the state to protect yourself from fines.

- Find out how to secure a prorated refund for your unused premium and prevent future rate hikes.

- Get the paperwork you need instantly by choosing a service that provides free junk car removal and immediate cash payments.

The Right Timing: When to Cancel Car Insurance After Junking a Car

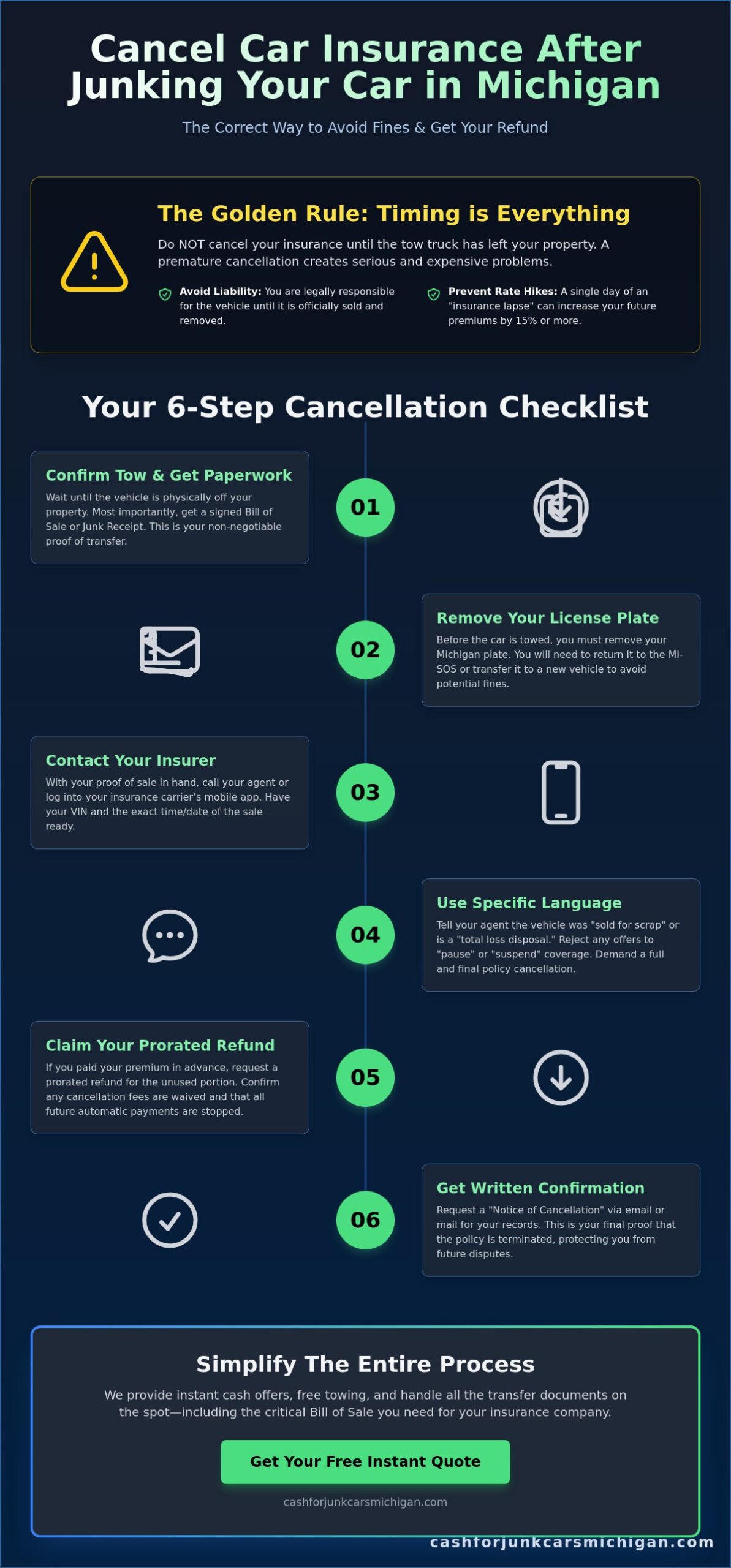

Don’t call your agent the second you decide to scrap your vehicle. It’s tempting to stop those automatic payments immediately, but rushing the process can cost you thousands in fines. You must keep your policy active until the vehicle is physically removed from your property. Liability remains with the registered owner until the Michigan Secretary of State (SOS) receives notification of the transfer. If a neighbor’s kid gets hurt near the car or a towing mishap occurs while it’s still on your policy, you need that coverage. The safe cancellation window is the specific moment the vehicle is off your property and all legal documentation is signed and in your possession.

Wait until the tow truck pulls away before you initiate the process of how to cancel car insurance after junking a car. Michigan law is clear about continuous coverage. If you cancel at 9:00 AM and the tow truck arrives at 2:00 PM, you have a five-hour window of illegal uninsured ownership. Insurance companies in 2026 use automated systems to flag these gaps. A single day of lapsed coverage can increase your future premiums by 15% or more. Stay protected until the deal is done.

Why Early Cancellation is a Legal Risk

Michigan requires No-Fault insurance for every vehicle registered in the state, even if it doesn’t run. An uninsured, non-running car is still a liability. If the vehicle rolls into the street or causes property damage during the loading process, the owner is responsible. Standard car insurance in the U.S. focuses on liability for a reason. Without it, you face “uninsured operation” fines from the Michigan SOS. These penalties often exceed the cost of keeping the policy active for one extra day. Don’t risk a court date to save ten dollars in premium costs.

The Junk Receipt: Your Proof of Sale

A professional buyer like Cash For Junk Cars Michigan provides more than just a stack of bills. We give you a signed receipt or bill of sale the moment we take the keys. This document is your shield. Your insurance agent needs this proof to backdate a cancellation or verify why the vehicle is no longer on your policy. There is a major difference between a standard title transfer and a scrap sale receipt. A scrap receipt proves the vehicle is being decommissioned, which helps insurers process your prorated refund faster. Keep this document for at least 18 months to ensure your driving record stays clean and your liability is fully terminated.

Step-by-Step: How to Properly Cancel Your Policy in Michigan

Once the tow truck pulls away with your vehicle, you need to act fast. You’ve already collected your cash payment, but your insurance company will keep billing you until you tell them to stop. Following the right process for how to cancel car insurance after junking a car ensures you don’t pay a penny more than necessary. Start by gathering your vehicle information. You need the VIN, the current mileage if known, and the exact date and time of the junk car removal. Having these details ready prevents back and forth delays with your insurance provider.

Contact your insurance agent or log into your carrier’s mobile app to initiate the request. You must provide the junk receipt or bill of sale as physical proof that you no longer own the asset. This is a critical step because insurers won’t just take your word for it. They need a paper trail to close the file. If you want to simplify this part of the process, sell your junk car for cash to a company that handles all the legal transfer documents on-site.

Contacting Your Insurance Carrier

Use specific terminology when you speak with your agent. Tell them the vehicle was a “total loss disposal” or was “sold for scrap.” These phrases are clear and leave no room for misunderstanding. Some agents might try to talk you into “pausing” the policy or switching to a “comprehensive only” storage plan. If you aren’t replacing the car immediately, reject these offers. Demand a full cancellation. Make sure the agent records the exact time the car left your property to ensure your coverage ends at that precise moment. This is also the time to confirm you’ve complied with Michigan SOS plate requirements by removing your tags before the tow.

Handling the Refund and Final Bill

Demand a prorated refund if you paid your premium in advance. In 2026, most Michigan insurers process these refunds via direct deposit or check within 14 days. Ask about cancellation fees. Some national carriers charge a small fee for ending a policy mid term, but they often waive this if you provide a scrap receipt. Confirm in writing that all future automatic withdrawals are cancelled. Finally, request a “Notice of Cancellation” for your records. This document proves the policy ended legally and protects you if the state questions your insurance status later.

Michigan State Requirements: SOS Notifications and Plate Returns

Michigan law mandates that you remove your license plates before any junk car leaves your driveway. This is not a suggestion. It is a legal requirement. In Michigan, license plates are tied to the individual owner rather than the vehicle itself. If you leave your tags on a car headed for the scrap heap, you remain linked to that VIN in the state’s database. This makes understanding how to cancel car insurance after junking a car even more critical. You cannot effectively stop your insurance payments if the state still thinks you are operating the vehicle on public roads. Proper plate disposal is the first step in proving to your insurer that the risk is gone. Learning the right way of how to cancel car insurance after junking a car starts with the SOS.

The Importance of Plate Removal

Plates are your personal property. Never leave them on a car going to a scrapyard. If that car is somehow involved in a crime or found abandoned, the police will come to your door first. Removing the plates also saves you money. You can transfer your old plates to a new vehicle for a small fee, usually between $10 and $15 in 2026. This is much cheaper than buying brand-new registration. It prevents third parties from misusing your identity and ensures your liability ends the moment the tow truck pulls away. If you don’t plan on buying a new car, destroy the plate. This prevents anyone from pulling it out of the trash and using it illegally. You should only cancel your policy after the plates are in your hands.

Notifying the Secretary of State (SOS)

Once the car is gone, the properly signed-over title serves as the legal transfer of ownership. Michigan does not require a separate liability release form, but notifying the SOS is a smart move. Use the Michigan SOS online portal to ensure the record reflects the sale. This is your protection against future parking tickets, toll violations, or abandoned vehicle fees. Michigan’s No-Fault insurance laws are strict. The state expects every registered vehicle to carry PIP and property protection. If the SOS doesn’t know you sold the car, they may flag you for an insurance lapse. This can lead to a suspended driver’s license or significant fines. If you need to sell my junk car but cannot find the title, don’t panic. Professional buyers can often handle the transaction with a bill of sale and a copy of your driver’s license. Completing this step proves to your insurance carrier that the asset is officially out of your name. This documentation is the final piece of the puzzle for stopping your premium payments without facing a state-mandated insurance lapse penalty. Get your cash, pull your plates, and notify the state the same day.

Avoiding the “Insurance Lapse” Trap and Other Pitfalls

A “lapse in coverage” is a major red flag for Michigan insurance carriers. If you cancel your policy and wait more than 30 days to get a new one, you’re categorized as a high-risk driver. Your rates can skyrocket by 35% or more when you finally buy your next vehicle. Many drivers learn how to cancel car insurance after junking a car but forget that the timing affects their future wallet. Michigan companies view a gap in your insurance history as a sign of financial risk. You lose your loyalty discounts. You lose your “continuous coverage” status. This mistake can follow you for three to five years, making your next car much more expensive to operate.

Don’t assume the insurance company knows the car is gone. They don’t. The Michigan SOS does not call your agent. The junkyard doesn’t send them a memo. If you stop paying your bill without a formal cancellation, your insurer will mark your account as “cancelled for non-payment.” This status tanks your insurance score and stays on your record. It’s much harder to get a fair rate later if you have a non-payment mark. If you want to avoid these headaches, sell your junk car for cash today and use that immediate payout to settle your final insurance bill properly.

What is a Non-Owner Policy?

A non-owner policy is a secret weapon for drivers who are between vehicles. It provides liability coverage for you as a driver, not for a specific car you own. This is the best option if you plan to buy another vehicle within six months. It keeps your insurance history active and proves you’re a responsible driver. It ensures you still have Personal Injury Protection (PIP) if you’re injured in someone else’s vehicle. Most importantly, it keeps your rates low for your next purchase. You stay in the “preferred” tier of customers because you never had a single day without coverage. In Michigan’s 2026 market, this small monthly cost saves you thousands in the long run.

The Myth of Automatic Cancellation

Stopping a bank transfer is not the same as canceling a policy. This is a dangerous pitfall that many people fall into. If you block the automatic withdrawal, the insurance company will continue to provide coverage for a short grace period. Then, they will cancel you for non-payment. This creates a legal lapse and a debt that can go to collections. Always call your agent directly. Provide the scrap receipt we give you. Confirm the exact date and time the policy ends. This proactive approach is the only way to ensure you don’t get hit with surprise bills or future rate hikes. Once you know how to cancel car insurance after junking a car the right way, you can move on without any financial baggage.

Junk Your Car for Cash Today and Simplify the Process

Getting that old vehicle off your property is the first step toward stopping those monthly insurance bills. Cash For Junk Cars Michigan provides the instant paperwork you need to finalize the process of how to cancel car insurance after junking a car. We don’t make you wait days for a check or a bill of sale. Our drivers provide a signed receipt on the spot, which is the exact proof your insurance agent needs to backdate your cancellation and process your refund. We buy any kind of car, truck, or SUV regardless of its condition. Whether it’s wrecked, rusted, or simply won’t start, we turn that liability into immediate financial relief.

Our service includes free junk car removal throughout the entire state of Michigan. You don’t have to worry about the logistics or the cost of hiring a private tow company. We handle all the heavy lifting and the legal paperwork so you can focus on your next vehicle. If you’ve been wondering how to cancel car insurance after junking a car without the headache of missing documents, we have you covered. We specialize in problem vehicles and frequently buy cars with no keys, no registration, or no title. We make the disposal process fast, simple, and profitable.

Why Choose Cash For Junk Cars Michigan?

We value your time and get straight to the point. We offer same-day pickup in Detroit and surrounding areas, ensuring your car is gone and your insurance is ready for cancellation before the sun goes down. Our pricing is 100% transparent. The cash quote we give you over the phone is the exact amount of cash you get when our driver arrives. There are no hidden fees for towing and no last-minute negotiations. We are the most reliable problem-solvers in the Michigan scrap market, providing a no-nonsense service that prioritizes speed and efficiency above all else.

Get Your Instant Quote Now

Stop paying for a car you can’t drive. Call us right now or fill out our online form for a fast, competitive offer. Once you accept the quote, prepare your vehicle for pickup by removing all personal items and taking off your license plates as required by Michigan law. Our driver will arrive on time, pay you cash on the spot, and tow your vehicle away for free. Get cash for junk cars today and stop paying for insurance you don’t need. It’s the fastest way to put money in your pocket and clear your driving record of unnecessary liabilities.

Take Control of Your Insurance Costs Today

You now have the exact 2026 roadmap for how to cancel car insurance after junking a car without getting hit by Michigan SOS fines or coverage gaps. Timing is your most important tool. Keep your policy active until the vehicle is physically off your property and you have a signed bill of sale in your hand. This simple step protects you from the 35% rate hikes that often follow a coverage lapse. Make sure you keep a copy of your reassigned title or bill of sale for at least 18 months as proof of the legal transfer.

Don’t let a non-running vehicle drain your bank account for another day. Cash For Junk Cars Michigan is ready to help you close this chapter fast. We provide same-day service across all of Michigan and include free towing with every pickup. Our driver will pay you cash on the spot and hand you the professional receipt you need to stop your premium payments immediately. Sell your junk car for cash today! It is time to clear your driveway and your monthly budget with one quick call.

Frequently Asked Questions

Can I cancel my car insurance if I lost the title to my junk car?

Yes, you can cancel your policy once the ownership transfer is complete. Professional buyers can often purchase your vehicle using a bill of sale and a copy of your driver’s license if the title is missing. Once you sign those ownership documents and the car is towed, you have the legal proof required to terminate your insurance coverage immediately.

Will I get a refund from my insurance company after I junk my car?

You are entitled to a prorated refund for any unused premium you paid in advance. Most Michigan insurance carriers in 2026 process these refunds within 14 business days via direct deposit or a mailed check. Ensure you provide the exact disposal date to your agent to maximize the amount of money returned to your bank account.

What happens if I forget to cancel my insurance after the car is scrapped?

You will continue to be billed for a vehicle you no longer own. Insurance companies do not receive automatic updates from scrap yards or the state. If you wait months to notify them, you may lose the ability to claim a backdated refund. You are essentially throwing away cash on a liability that no longer exists.

Do I need to tell the Michigan SOS that I junked my car?

Yes, you should notify the Michigan Secretary of State through their online “Record of Sale” portal. This step officially informs the state that you are no longer responsible for the vehicle’s registration or mandatory No-Fault coverage. It prevents the state from flagging you for an insurance lapse on a VIN that has already been crushed.

Should I keep insurance on a car that doesn’t run?

You must maintain insurance as long as the vehicle is registered and has valid license plates. Michigan law requires Personal Injury Protection (PIP) for all registered vehicles regardless of their mechanical condition. To stop paying, you must first junk the car and then follow the proper steps for how to cancel car insurance after junking a car to stay legal.

How much does it cost to cancel a car insurance policy in Michigan?

Most companies do not charge a flat fee for cancellation, but some may apply a “short rate” penalty. This is typically a small percentage of your remaining premium if you cancel mid-term. Ask your agent for a final statement to confirm if any small administrative fees apply to your specific policy before you close the account.

Can I transfer my insurance policy from my junk car to a new one?

Yes, transferring your policy is often smarter than a full cancellation. Your agent can simply swap the VIN of your junk car for your new vehicle’s information. This maintains your “continuous coverage” status and protects your loyalty discounts. It is the most efficient way to handle how to cancel car insurance after junking a car while staying insured.

What proof does the insurance company need that I sold the car for scrap?

Insurers require a signed scrap receipt or a bill of sale that clearly shows the vehicle’s VIN and the date of the transaction. This document proves the asset is no longer in your possession. We provide this paperwork the moment we pay you cash, giving you the immediate evidence needed to fax or email your agent.